The HPC Settlement of $ 3b of Cipher Mining (CIFF) ought to have been a catalyst, however the motion was on the aspect when an convertible improve of $ 1.3B stole the main target of consideration. Right here is why establishments rushed and what it means to shareholders.

The next visitor publication comes from Bitcoinminingstock.io, A public market intelligence platform that delivers knowledge on firms uncovered to Bitcoin’s mining and cryptographic methods. Initially printed on October 1, 2025 by Cindy Feng.

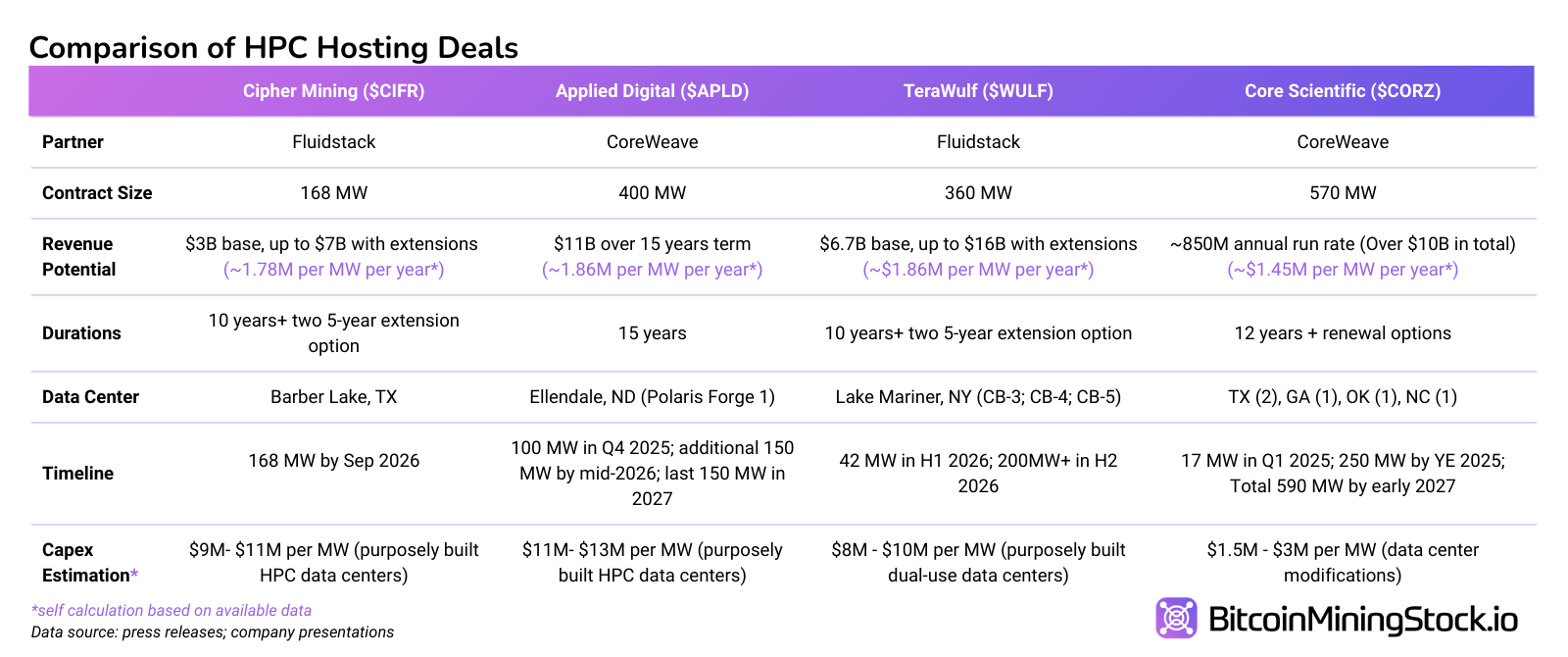

Lately encryption mining introduced His first Hyperscala settlement, revealing Fluidstack as his HPC consumer, the identical accomplice backed by Google Terawulf signed earlier this yr. This marks the fourth largest HPC lodging contract between public miners, reinforcing the sector pivot in HPC as a complement to Bitcoin mining.

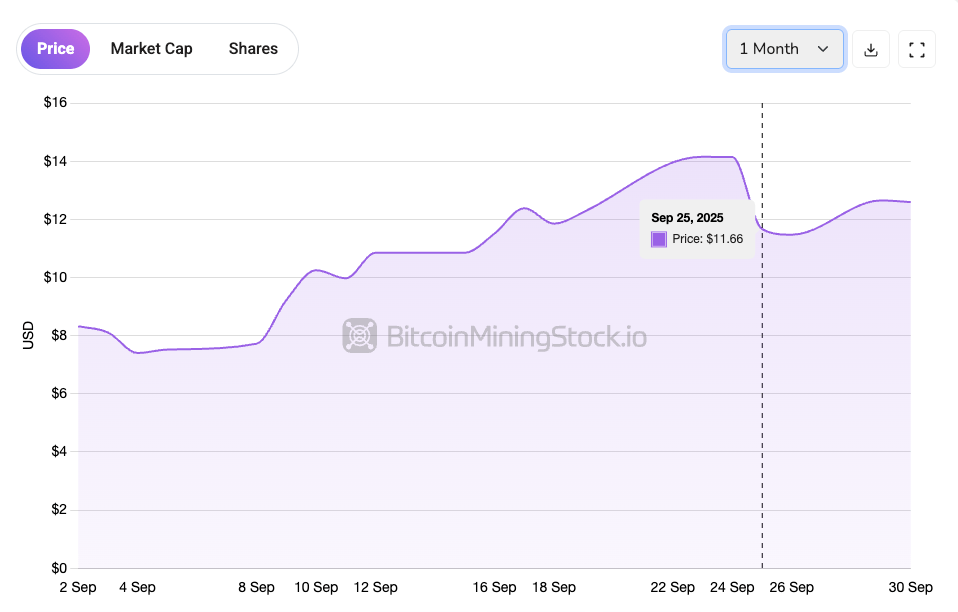

Usually, such adverts trigger a sustained rally. This time, Cipher’s actions initially elevated, however they rapidly fell after presenting a fantastic non-public financing. Inside 24 hours, a Non-public Convertible Notes Workplace of $ 800 million Relieved a $ 1.1 billion On an amazing institutional demand. In social networks, traders blamed the convertibles for killing the impulse. This notion is comprehensible, however additionally it is a reminder that robust preliminary prices are required in order that HPC/AI income are actual.

Now we unpack the mechanics of this financing settlement, as a result of we are going to uncover why the establishments rushed and the shareholders reacted cautiously.

HPC Economics and the monetary hyperlink

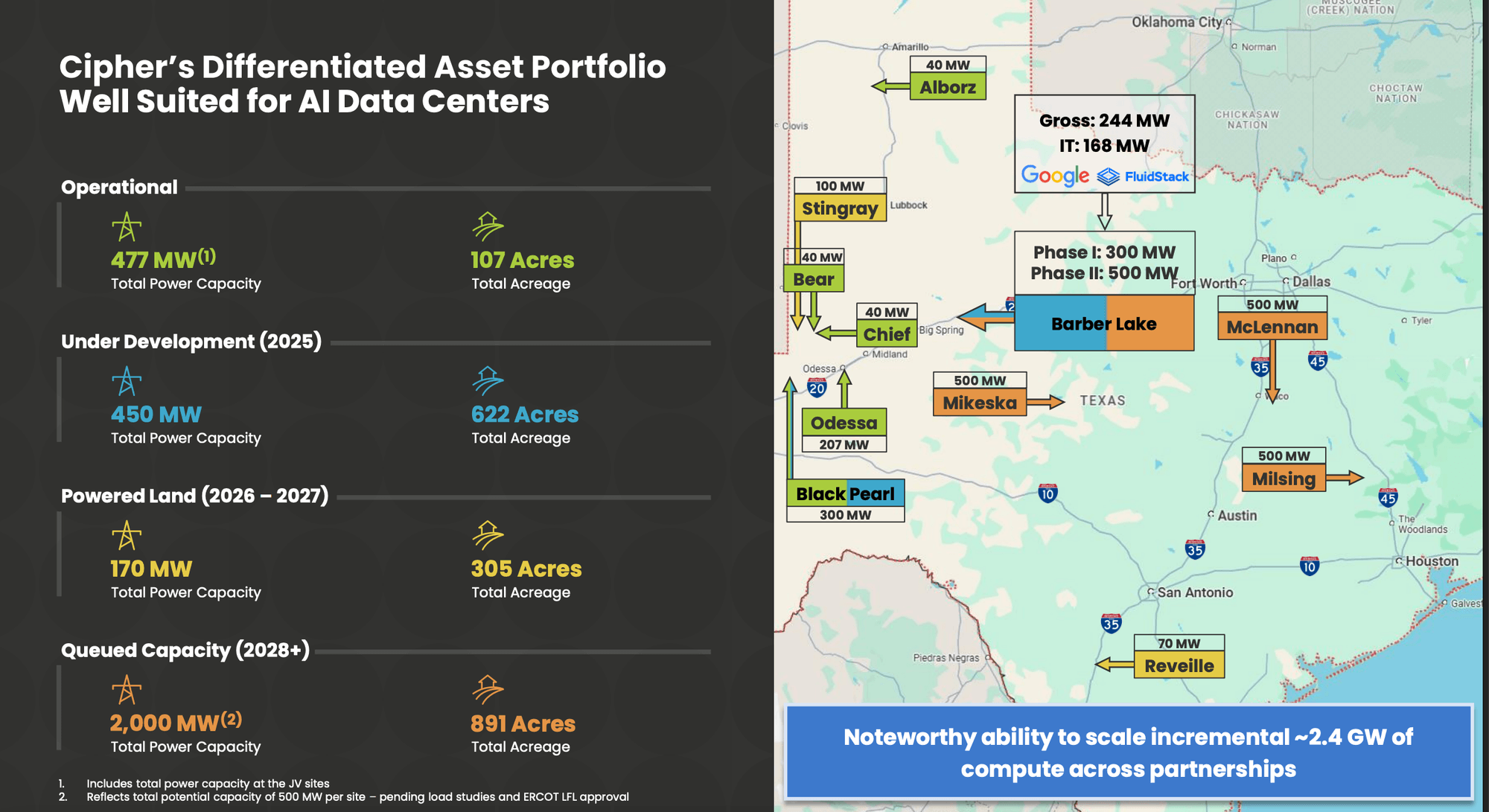

The Barber Lake and probably the most broad CIPHER 2.4 GW pipe web site are the spine of its HPC technique. Internet hosting Hyperscalers requires Mass preliminary bills On land, interconnection of vitality and building of the information heart. The fluidstack contract validated the demand, however the capital was the bottleneck.

*It’s anticipated that the development of Barber Lake 168MW solely requires roughly $ 1.5B – $ 1.8B in CAPEX, even earlier than making an allowance for the extra expense essential to fully make the most of the broader vitality portfolio of CIPHER.

That is the place the convertibles enter. The rise of $ 1.1b will not be a final second concept for the historical past of HPC, it’s a vital step. By making certain the capital of lengthy knowledge with zero curiosity, Cipher purchased the time and assets to execute. Nonetheless, in doing so, administration modified the danger of operations to the construction of fairness.

Breaking the convertible notes

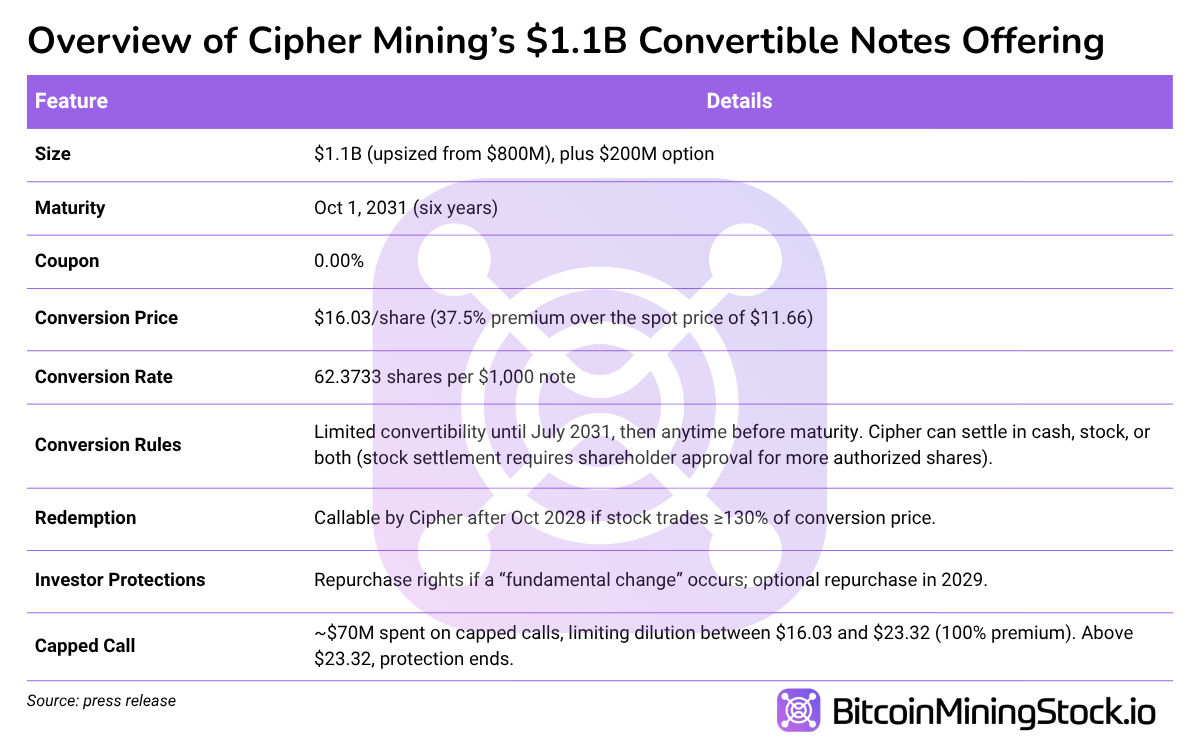

Determine 0.00% of main convertible notes expired on October 1, 2031Scheduled to determine itself on September 30, 2025. The settlement was decreased from $ 800 million to $ 1.1 within the time instantly, with an extra choice of $ 200 million*, which mirrored the overwhelming institutional demand.

*The acquisition choice of $ 200 million was exercised, per encryption 8-Ok typebringing the full convertible notes issued to $ 1.3 billion.

In relation to see miners, the settlement (6 -year funds at an rate of interest of 0%) appears low cost. Some have paid 10%+ rates of interest for money owed or have trusted the issuance of collection capital. Along with that, Cipher intends to make use of $ 70 million to finance the price of coming into the Restricted name transactionsIt helps cut back dilution if the inventory will increase. In different phrases, shareholders are protected against dilution to $ 23.32 per share (virtually 2 occasions the sale worth reported on September 25, 2025).

Why establishments rushed

At first look, this non-public provide, with out curiosity and is blocked till 2031, appears unattractive. However a convertible notice will not be a easy hyperlink, it’s basically a Mortgage plus a purchase order choice in motion. Buyers receive the reimbursement of the torque in 2031 if the struggles just like the encryption struggle, but when the motion will increase above $ 16.03, they’ll change into capital and seize upwards.

For protection funds, attraction goes past easy lengthy -term publicity. Many run Convertible arbitration methodsthe place they purchase the notes and a brief inventory in proportion to the conversion ratio. The quick hedge is then dynamically adjusted As the value of shares progresses. The target is to not guess on the basics of an organization, however to learn from the construction and volatility just like the choice of actions.

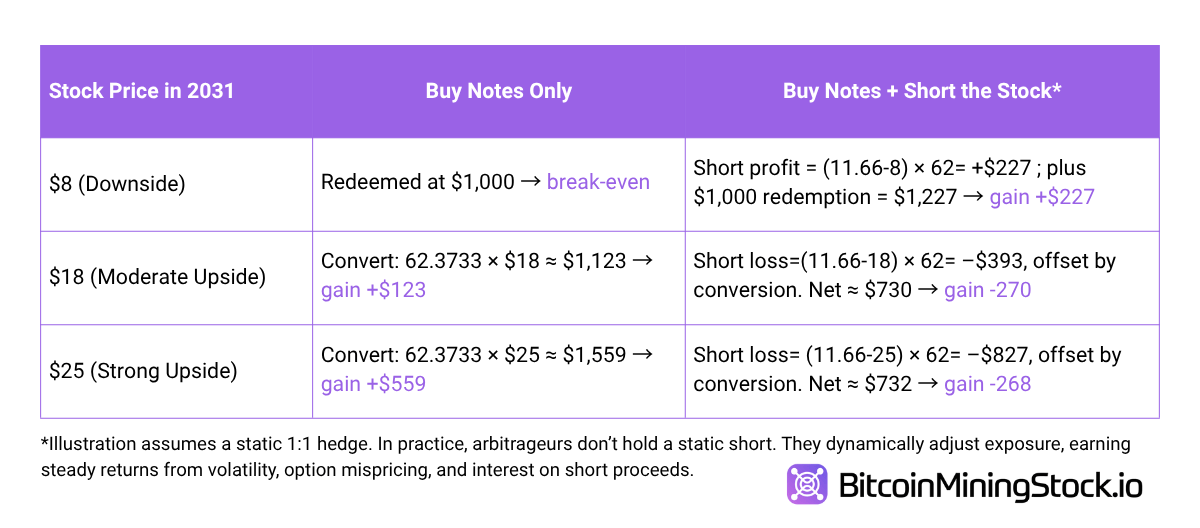

For example, suppose an investor buys $ 1,000 nominal worth of notes (62,3733 actions in the event that they change into). Cipher’s shares value $ 11.66; The conversion is $ 16.03.

With a Static configurationThe outcomes could be seen as:

So what does this imply? Though static arithmetic appear unattractive for arbitrations at increased costs, dynamic protection is what makes the technique worthwhile among the many outcomes. That’s the reason establishments accumulate: they receive a construction that gives Safety just like a hyperlink with benefitWhereas frequent shareholders solely win if Cipher runs efficiently. This explains why the settlement was elevated in a matter of hours.

How dilution works for shareholders

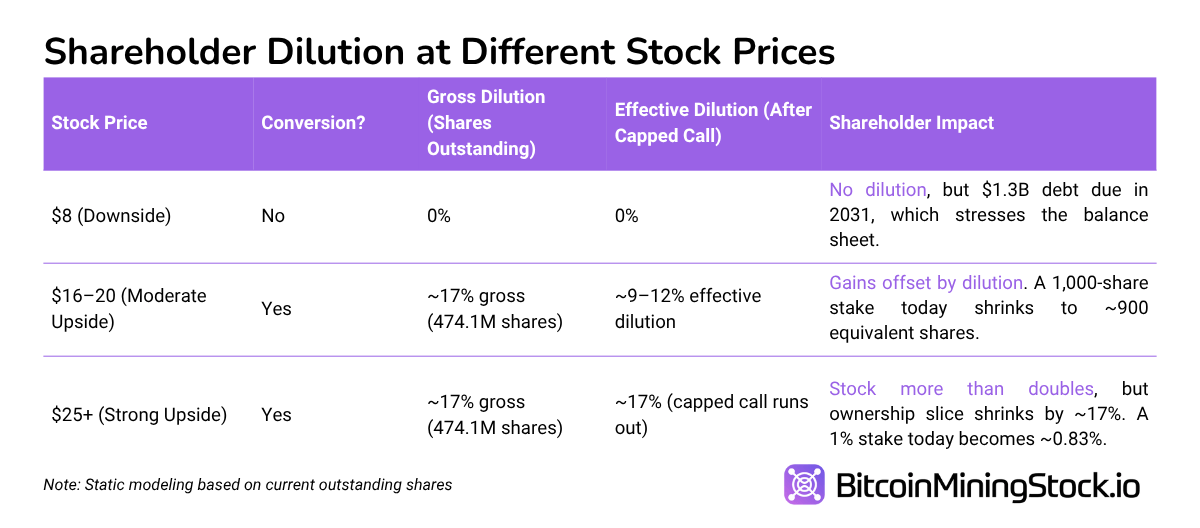

For frequent shareholders, the impression is straightforward and far much less versatile than for establishments. Cipher at the moment has ~ 393m actions in circulation. If all notes change into, new shares will likely be issued, elevating the full to ~ 474.1m, a dilution of 17%. The restricted name cuts this to 9-12% If the shares land between $ 16.03 and $ 23.32, however past that (> $ 23.32) the safety is exhausted and the shareholders take up the entire dilution.

Asymmetry Right here: establishments can alter their threat and block returns via protection, however shareholders can not. Capital traders have a binary outcome: Cipher is executed and the motion appreciates sufficient to exceed 9-17% of the dilution, or doesn’t, they usually maintain a weaker motion plus $ 1.3b of debt that hangs on the corporate.

Ultimate ideas

Cipher Fluidstack Contract validated Its strategic change in HPC and lodging of AI. Like Core Scientific, Appliad Digital and Terawulf, the corporate is profiting from vitality and infrastructure to draw Hipperscala prospects, pointing to revenue flows which are way more predictable than Bitcoins pure mining.

Nonetheless, the silenced inventory response reveals how financing It might eclipse even probably the most constructive headlines. Convertible notes of $ 1.3 billion, intelligently structured with out quick money drainage and safety of restricted calls, nonetheless characterize a considerable future declare on capital. Shareholders face a 9 to 17% dilution if encryption is executed, however that Dilution would solely attain considerably increased actions costs.

This pressure explains divergence: the HPC Deal is a transparent strategic victoryHowever the financing reformulated the investor method to the danger. Cipher is by capital entrance to construct Barber Lake and activate its 2.4 GW pipe, a vital step if you wish to monetize the HPC demand at scale. If the execution arrives in time and the 168 MW of Barber Lake are on-line in September 2026 as deliberate, the ensuing revenue may exceed the dilution.

For now, convertibles give establishments a low threat and choice entry level, whereas shareholders entail the danger of execution. The HPC story continues to be convincing, however till tangible revenues materialize, the market will see an encryption much less for its fluid settlement and extra for the financing of $ 1.3 billion that you just used to finance it.