Crypto-backed borrowings surged to a file $73.6 billion within the third quarter, making it probably the most leveraged quarter ever for the sector, however the leverage combine seems to be considerably more healthy than throughout the 2021-2022 cycle.

In line with Galaxy Analysis, this sharp rise is overwhelmingly pushed by on-chain lending, which now accounts for 66.9% of all crypto-backed debt, up from its earlier peak of 48.6% 4 years in the past.

DeFi lending alone rose 55% to a file excessive of $41 billion, supported by points-driven consumer incentives and improved collateral varieties resembling Pendle Principal Tokens.

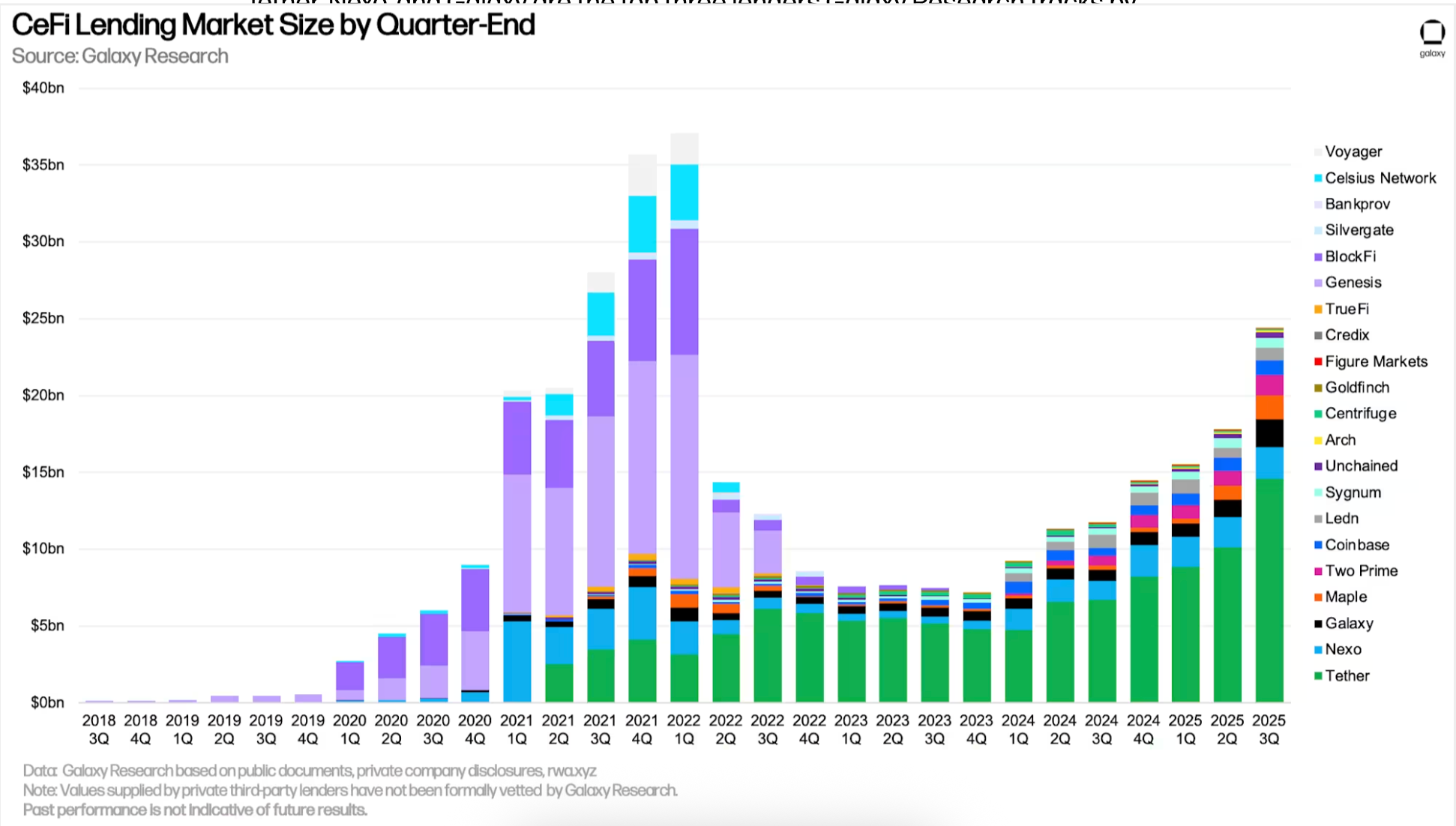

Centralized monetary establishments additionally confirmed a restoration, with borrowings up 37% to $24.4 billion, however the market stays one-third the dimensions of its 2022 peak.

Concentrated mortgage graph (Galaxy Analysis)

Corporations that survived the final cycle have largely deserted unsecured lending and are turning to totally collateralized fashions that search institutional traders and public listings. Tether stays the dominant CeFi lender, holding practically 60% of tracked loans.

This quarter additionally noticed decisive modifications in DeFi itself, with lending apps capturing over 80% of the on-chain market and CDP-backed stablecoins shrinking to 16%. New chain developments resembling Aave and Fluid on Plasma have spurred exercise, with Plasma elevating greater than $3 billion in debt inside 5 weeks of launch.

It’s price noting {that a} leveraged wipeout occurred shortly after the top of the third quarter, leading to over $19 billion price of liquidations, making it the biggest single-day cascade in crypto futures historical past.

Nonetheless, Galaxy’s report maintains that the liquidation incident doesn’t mirror systemic credit score weak spot, saying that almost all positions had been mechanically de-risked because the alternate’s computerized deleveraging system was activated.

In the meantime, company digital asset treasury (DAT) methods proceed to depend on leverage, with excellent debt related to crypto acquirers exceeding $12 billion. Complete trade debt, together with DAT issuance, reached $86.3 billion, a file excessive.

Information means that leverage in cryptocurrencies is rising once more, however on a stronger and extra clear foundation, with collateralized constructions changing the opaque and unbacked credit score that fueled the final boom-bust cycle.