CleanSpark has signed a 20-year AI infrastructure lease, however nonetheless must finance an estimated $1.75 billion to $2.1 billion knowledge middle buildout.

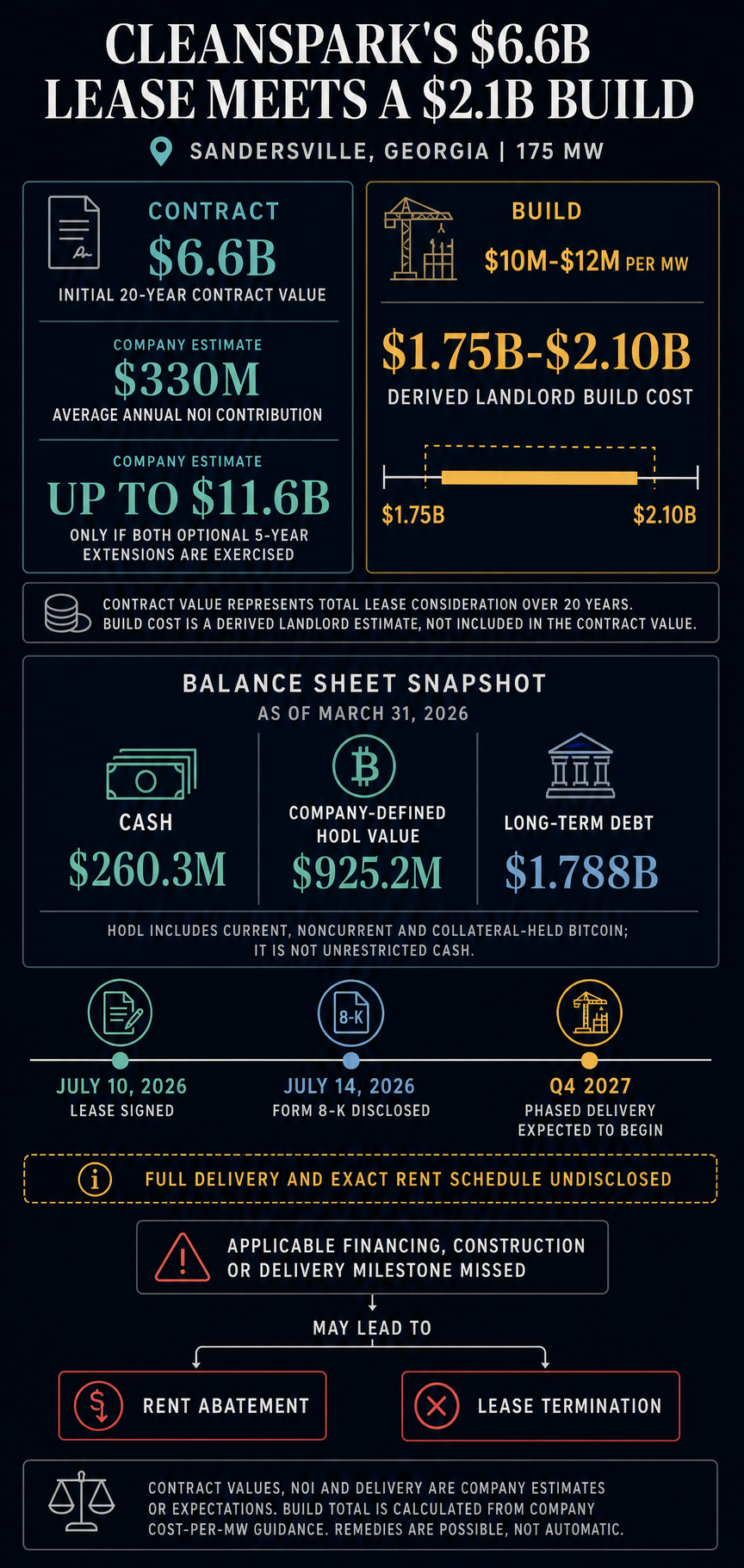

The Bitcoin miner and knowledge middle developer entered right into a 20-year triple web lease for 175 megawatts of important IT load at its Sandersville, Georgia, campus on July 10. CleanSpark disclosed the deal in a Type 8-Ok on July 14 and estimates the preliminary time period can have a contract worth of $6.6 billion and can contribute about $330 million in common annual web working revenue.

CleanSpark’s estimate of $10 million to $12 million in challenge prices to householders per MW implies building of $1.75 billion to $2.1 billion.

That vary exceeds the $260.3 million in money and $925.2 million in company-defined Bitcoin HODL worth reported as of March 31, 2026, even when the 2 figures are added. The HODL measure contains present and non-current Bitcoin, in addition to Bitcoin held by counterparties underneath collateral preparations, a distinct composition than unrestricted money.

The July leasing announcement doesn’t determine any lender, financing quantity dedicated, worth, sponsor capital contribution or drawdown schedule. Phased supply is anticipated to start within the fourth quarter of 2027, whereas full supply and leasing begin schedules stay undisclosed. CleanSpark says the unnamed tenant’s high-investment-grade credit score profile makes it simpler to entry financing. The ultimate phrases will decide whether or not the challenge is primarily financed towards the lease or imposes extra leverage, dilution or Bitcoin collateral threat on the corporate and its shareholders.

What CleanSpark truly signed

The Sandersville settlement is a binding infrastructure lease protecting 175 MW, with annual escalators, an preliminary time period of 20 years and two non-obligatory five-year extensions. The tenant is described solely as a high-investment grade international know-how firm, whose identification shouldn’t be being disclosed.

CleanSpark estimates $6.6 billion in contract worth over the preliminary time period and as much as $11.6 billion if each five-year choices are exercised. The initially signed time period continues to be $6.6 billion; Reaching $11.6 billion requires the train of each choices.

Calling it a triple-net lease doesn’t suggest CleanSpark can be concerned in constructing the challenge. The 8-Ok states that the tenant bears the prices, costs, indemnities and bills specified within the lease. CleanSpark individually estimates the proprietor’s challenge prices between $10 million and $12 million per MW within the SEC submitting, leading to an estimated vary of $1.75 billion to $2.10 billion for 175 MW.

The contract worth is unfold over years, whereas the estimated NOI stays potential. A phased building program might also not require all the challenge price up entrance. The figures set up the size of the duty with out revealing when every greenback should be funded.

Financing channels transfer threat in a different way

CleanSpark’s fiscal second-quarter outcomes present why Sandersville wants financing to match the size of building.

As of March 31, the corporate reported $260.3 million in money, $925.2 million in HODL worth, $1.788 billion in long-term debt, and $1.927 billion in whole liabilities. Sandersville’s calculated price is roughly 6.7 to eight.1 occasions dated money stability, 1.9 to 2.3 occasions HODL and roughly 98% to 117% long-term debt. These figures present that the challenge is just too huge for CleanSpark to fund with its current money.

CleanSpark additionally reported a web lack of $378.3 million for the quarter ended March 31. The determine included a $224.1 million Bitcoin truthful worth loss and a $38.8 million loss in Bitcoin collateral, in line with its earnings launch filed with the SEC. These market-linked gadgets can considerably affect the reported stability sheet, making web loss a poor indicator of quarterly money burn.

Bitcoin stays a possible supply of liquidity, collateral or proceeds from the sale, relying on how a lot it’s taxed and the extent of publicity the corporate needs to keep up. Cash pledged to a lender can’t additionally operate as an unencumbered reserve. CryptoSlate beforehand examined how collateralized Bitcoin complicates the liquidity implied by CleanSpark’s headline HODL determine.

A believable state of affairs is the financing of the challenge constructed across the website and its tenant-backed lease. CleanSpark says the tenant’s credit score profile facilitates financing choices, and a long-term lease can present lenders with a contractual money circulate base to finance building. Protections would rely upon the precise package deal: sponsor ensures, company sources, Bitcoin collateral, or a big capital dedication from the sponsor may shift the chance again to CleanSpark.

The lease ties financing on to CleanSpark’s potential to execute the challenge. CleanSpark’s 8-Ok states that the corporate should adjust to relevant financing, building and supply milestones, in addition to different covenants and circumstances. If a milestone is missed, the lease might be lowered or disappear totally, leaving challenge financing tied to CleanSpark conserving the lease in place.

Financing Sandersville by way of CleanSpark’s company stability sheet would expose shareholders extra on to the price. The extra company debt would improve leverage from a March 31 base of practically $1.8 billion in long-term debt. New frequent fairness or equity-linked securities may dilute current holders. Bitcoin gross sales would scale back treasury publicity and buyers’ asset base might be counted as liquidity. Bitcoin-backed loans may protect nominal possession of the forex whereas including collateral, margins, and liquidation dangers.

CleanSpark’s web ebook stability of $1.769 billion for zero-coupon convertible notes represents excellent debt. Its $400 million in unused Bitcoin-backed credit score strains have been undrawn as of March 31 and require Bitcoin collateral. CryptoSlate’s protection of the 2025 convertible financing gives context for the company path, whereas Hut 8’s AI proprietary mannequin illustrates how challenge debt and Bitcoin-backed bridge capital can coexist. The ultimate construction of CleanSpark stays an open query.

The tenant’s credit score profile might assist challenge financing, however eventual worth, recourse, collateral and fairness necessities will decide how a lot threat stays with CleanSpark.

Why the worth of $6.6 billion continues to be conditional

The $6.6 billion headline nonetheless comes with strings hooked up. The financing, building, supply and different milestones and agreements disclosed within the 8-Ok tie the income alternative to CleanSpark’s potential to execute. The cures are conditional: the submitting states that relevant failures might end in lease reductions or termination.

The timeline provides one other disadvantage. CleanSpark expects phased deliveries to start within the fourth quarter of 2027. It has not disclosed how shortly the complete 175 MW will observe, when leasing will start for every section, or whether or not the said annual common NOI displays a completely delivered campus. Utilizing $330 million as a run price from the primary day of This fall 2027 would overstate the revealed timeline.

The Texas settlement shouldn’t be a part of the portfolio of contracts signed by CleanSpark. The identical tenant executed a letter of intent and exclusivity settlement protecting CleanSpark’s 718-acre Texas portfolio and as much as 885 MW of what CleanSpark describes as secured and deliberate energy capability. That settlement shouldn’t be an entire lease.

Sandersville has superior CleanSpark from an AI infrastructure launch to contract execution, whereas decisive capital phrases stay undisclosed.

The financing phrases and path to This fall 2027 will reveal who is de facto in danger: CleanSpark’s Bitcoin holdings, its stability sheet, or its shareholders.