Bitcoin is making deeper inroads into U.S. family budgets as homebuyers weighed down by excessive borrowing prices and restricted provide search new methods to boost down funds with out promoting their digital belongings.

On March 26, Higher Dwelling & Finance and Coinbase launched a scheme that permits eligible debtors to pledge Bitcoin or the USD Coin (USDC) stablecoin to take out a standards-compliant mortgage mortgage whereas securing one other mortgage as a down cost.

The deal would introduce cryptocurrencies to one of many hottest components of the U.S. credit score system at a time when affordability pressures are already reshaping who should buy properties and when.

The timing is central to the pitch, as Realtor.com’s 2026 report pegs the U.S. housing provide hole at 4.03 million models.

This comes as the common rate of interest for a 30-year mortgage not too long ago rose to 7%, whereas whole mortgage purposes fell by 10.5% and buy purposes fell by 5.4%. On the similar time, first-time patrons make up simply 21% of the market, in line with the Nationwide Affiliation of Realtors’ newest profile.

In opposition to this backdrop, lenders and crypto corporations imagine {that a} rising group of potential patrons have wealth in digital belongings however lack the money liquidity wanted to beat one of many largest obstacles to homeownership.

A brand new route into the mortgage market

The Coinbase-backed product is aimed toward debtors who wish to keep publicity to the cryptocurrency market slightly than liquidating their holdings to boost money for a down cost.

For a lot of, that call is extra necessary than market timing. Promoting cryptocurrencies may set off tax payments and pressure traders to cut back positions they take into account long-term.

With this in thoughts, the construction is structured round two loans at closing. The primary is an ordinary mortgage on actual property. The second is a personal mortgage backed by collateralized cryptocurrencies, which is used as money for the down cost.

Vetter mentioned 15-year and 30-year mounted mortgage choices can be found, topic to credit score approval, and the mortgage is designed in accordance with Fannie Mae tips and the mortgage stays a conforming mortgage.

That distinction is necessary. This product is just not supposed to exchange a standard house mortgage with a cryptocurrency mortgage. As an alternative, it leaves the first mortgage in its conventional kind and wraps a cryptocurrency-backed financing layer across the down cost.

For debtors utilizing Bitcoin, the preliminary collateral worth should be at the very least 250% of the mortgage quantity in fiat forex. For debtors utilizing USDC, the preliminary collateral worth should be at the very least 125%.

From a sensible standpoint, a borrower can pledge $250,000 in Bitcoin to unlock a $100,000 money down cost mortgage, or $125,000 in USDC to realize the identical consequence.

The businesses are selling the deal as a method to keep possession of digital belongings whereas getting access to the housing market. Higher says each loans can share the identical rate of interest and amortization interval, making a single mixed month-to-month cost.

A spot is created attributable to distortion within the housing.

The product’s attraction is instantly tied to a housing market that has change into tougher to interrupt into, particularly for youthful patrons.

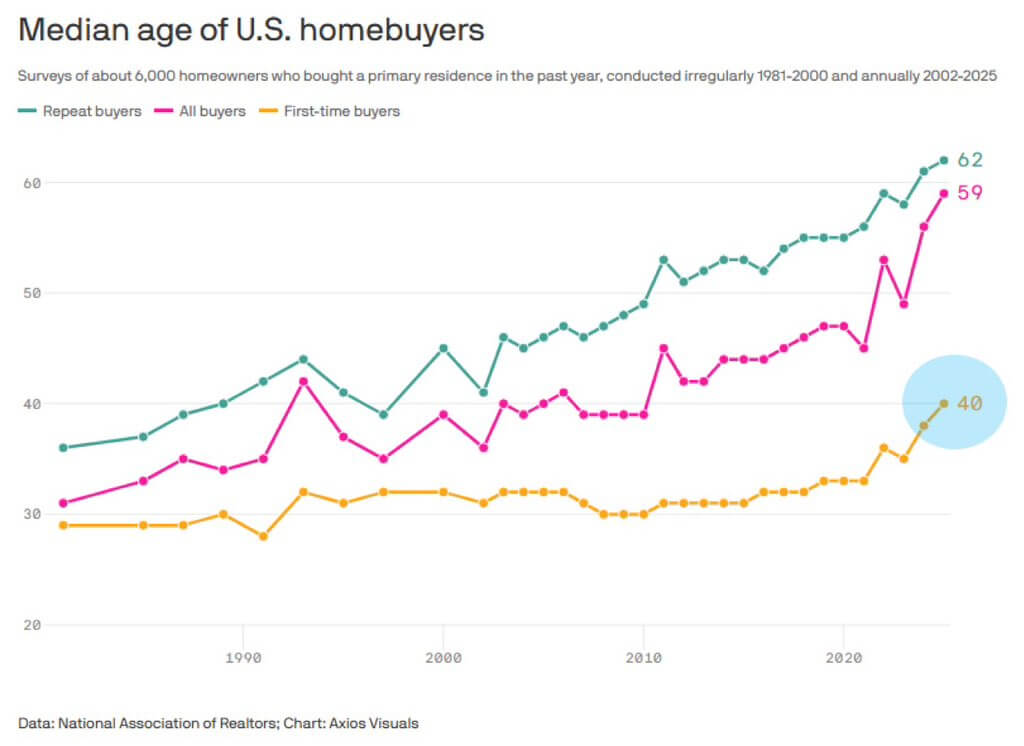

The median age of first-time homebuyers will attain 40 by 2025, reflecting the mixed results of excessive mortgage charges, rising house costs and restricted stock, in line with the Nationwide Affiliation of Realtors.

For households with decrease incomes, the stress is much more extreme. The NAHB/Wells Fargo Housing Price Index for the second quarter of 2025 confirmed {that a} typical household would want 36% of their revenue to pay the mortgage on a median-priced new house. Amongst low-income households, the proportion exceeded 71%.

These numbers assist clarify why corporations are seeing a possibility to attach digital belongings to house finance. Conventional underwriting depends closely on documented revenue, credit score historical past, and money reserves.

This framework tends to favor households which have already constructed wealth by house fairness, revenue progress, or long-established monetary belongings.

On the similar time, thousands and thousands of People are constructing positions in cryptocurrencies. For comparability, about 20% of adults in america (that is 52 million folks) personal some form of cryptocurrency, and the vast majority of them are younger folks.

The NCA 2025 State of Crypto Holders report confirmed that 67% of token holders are below the age of 45 and 26% have an annual revenue of lower than $75,000.

This offers this product a transparent goal market. That’s, younger patrons who’ve enough publicity to cryptocurrencies, however who’ve restricted want or means to transform their holdings into money on the time of buy.

How cryptocurrency pledges work

The businesses are attempting to make the product extra of a mortgage-compatible financing device than a risky cryptocurrency mortgage.

Debtors collateralizing Bitcoin or USDC will not be topic to margin calls or top-up necessities, even when the market worth of the collateral declines.

It’s higher to say that market actions alone don’t trigger liquidations. Moderately, the businesses mentioned the pledged belongings are solely in danger if the borrower is 60 days behind on funds, a threshold that mirrors the remedy of cost stress in conforming mortgages.

The cryptocurrency is saved for the lifetime of the down cost mortgage and returned as soon as the duty is repaid. Debtors can not commerce whereas the pledged asset is locked, sustaining possession however limiting flexibility.

For USDC debtors, stablecoins can proceed to earn rewards, which may assist offset mortgage reimbursement prices and scale back the substantial financing burden for debtors.

In the meantime, our broader ambitions prolong past one mortgage product. Higher and Coinbase say they intend to develop the scope of eligible digital belongings over time to incorporate tokenized shares, bonds, and different tokenized actual property belongings.

This can be a signal that they see their mortgage providing as an early step in bringing on-chain wealth into mainstream client finance.

Coverage help and political resistance

In the meantime, the launch comes amid a political local weather that’s more and more receptive to cryptocurrencies, however not with out resistance.

Fannie Mae’s function and the Federal Housing Finance Company’s oversight may assist make these merchandise extra mainstream than earlier crypto-linked mortgage merchandise.

Final yr, FHFA Secretary Invoice Pulte directed Fannie Mae and Freddie Mac to arrange to depend cryptocurrencies as belongings in mortgage purposes, reflecting the Trump administration’s broad help for the digital asset trade.

The coverage opening has created room for business merchandise constructed round crypto belongings, however has additionally drawn criticism from lawmakers who see the concept as a brand new supply of danger for housing finance.

Democratic senators led by Elizabeth Warren opposed the proposal, arguing that present coverage doesn’t permit federally backed mortgage channels to contemplate cryptocurrencies except they’re first transformed to U.S. {dollars} and correctly documented.

They warned that increasing underwriting requirements to incorporate non-convertible digital currencies may introduce new dangers to each the housing market and the broader monetary system.

This criticism is on the coronary heart of discussions about merchandise like Higher’s.

Proponents see this as a method to convert digital belongings into real-world entry with out forcing debtors to promote their belongings or exit the market. Critics see the hazard in bringing a risky and growing asset class nearer to the bottom of U.S. house lending.

The final word end result might due to this fact depend upon whether or not crypto-backed mortgages stay a distinct segment device for rich digital asset holders or evolve right into a broader financing channel for patrons shut out by conventional down cost hurdles.

(Tag translation) Bitcoin