Banks are more and more turning to tokenized deposits as they embrace blockchain know-how to enhance the way in which cash strikes by the monetary system. A brand new report from Arcam Intelligence says regulated banks are creating digital variations of buyer deposits that function on blockchain networks however stay on the financial institution’s stability sheet.

This transition will enable banks to automate transactions sooner and with out disrupting the important structure of conventional banking. In distinction to stablecoins, tokenized deposits stay financial institution liabilities and are regulated in keeping with banking laws.

What tokenized deposits really do

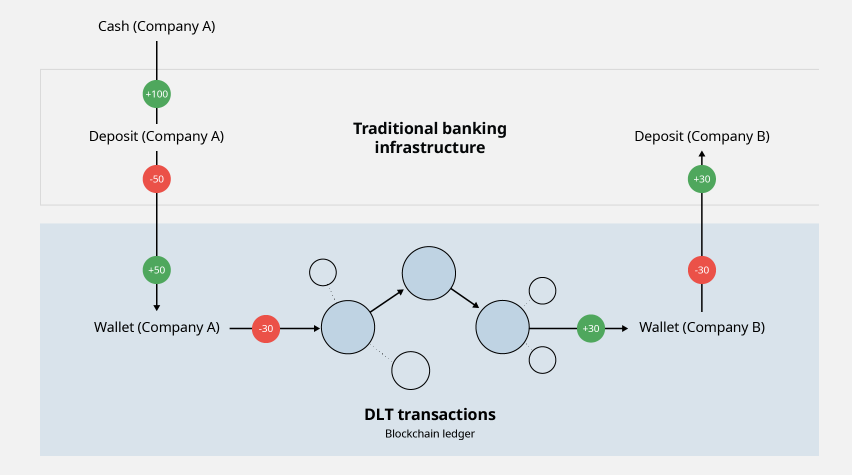

Tokenized deposits are a digital model of financial institution deposits that run on a blockchain community. The deposit stays with the regulated financial institution, however the buyer receives a digital token representing the identical worth. This enables banks and companies to maneuver funds extra rapidly than conventional cost methods, which depend on financial institution enterprise hours and sometimes take longer to settle transactions.

The know-how additionally permits banks to automate funds based mostly on pre-agreed phrases. For instance, firms can transfer funds between subsidiaries at any time or mechanically launch funds after invoices are accredited or liquidity targets are reached.

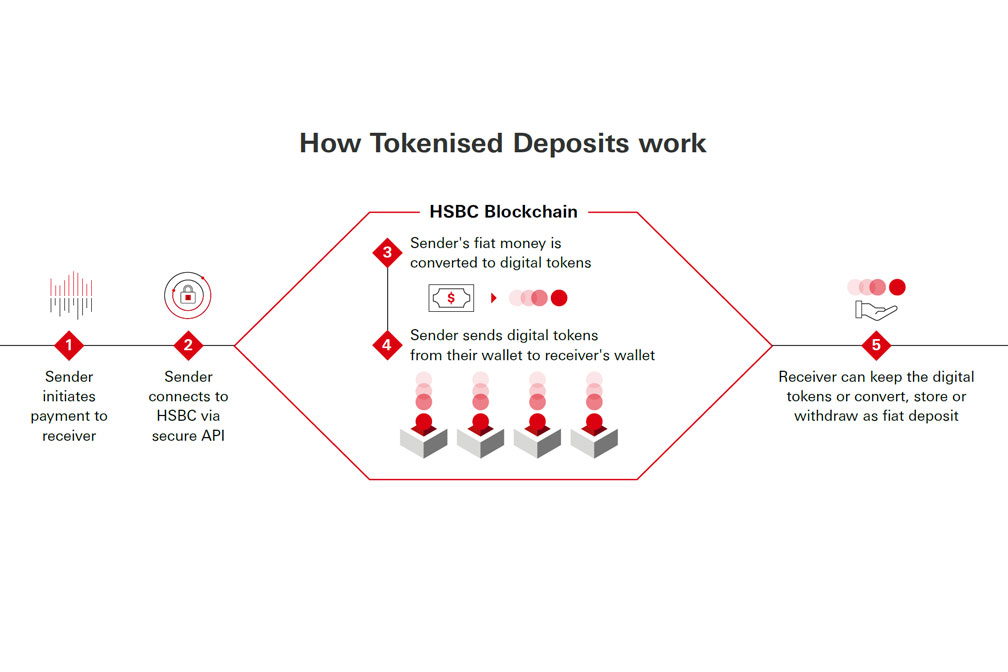

In September 2025, HSBC accomplished the primary cross-border tokenized deposit transaction between Hong Kong and Singapore for Ant Worldwide, demonstrating how the know-how works. The transaction reduces delays brought on by time zone variations and permits the corporate to handle its monetary operations extra effectively.

Why is it completely different from steady cash?

Tokenized deposits are sometimes in comparison with stablecoins as a result of they use blockchain know-how to maneuver digital cash. Nevertheless, in keeping with Arkham Intelligence, the 2 work in very alternative ways.

Stablecoins reminiscent of USDT and USDC are issued by non-public firms that again their tokens with reserve property. In keeping with knowledge from rwa.xyz, the excellent quantity of USD-denominated stablecoins up to now is anticipated to succeed in almost $300 billion by mid-2026.

In distinction, tokenized deposits are issued by regulated banks and signify buyer deposits that these establishments already maintain. Additionally it is solely out there to licensed shoppers by permissioned blockchain networks.

A February 2026 report by the New York Fed highlighted that stablecoins are supposed to function “protected cash,” whereas tokenized deposits turn out to be a part of the normal banking system and are helpful for financial institution lending.

Main banks drive business adoption

A serious international monetary establishment has launched a tokenized deposit system because it continues to undertake blockchain know-how. Among the business’s largest gamers embody JPMorgan by its Kinexys system, previously often known as Onyx. Kinexys methods have executed greater than $7 billion in transactions day-after-day since its inception, with greater than $3 trillion processed.

HSBC has expanded its tokenized deposits to Hong Kong, Singapore, UK, Luxembourg, and US territories. The system helps a wide range of currencies and allows automated funds and settlement of tokenized deposits.

One other participant that joined the business in January 2026 was BNY Mellon, which launched a tokenized deposit product geared toward establishments. It has additionally invested in blockchain infrastructure whereas taking up tasks associated to tokenized cash market funds.

Challenges that also require options

Regardless of the rising reputation of tokenized deposits, the know-how faces a number of hurdles. At the moment, the platform runs inside one financial institution’s ecosystem, and tokenized deposits can’t be transferred from one monetary establishment to a different with out leaving the system. To resolve this downside, the clearinghouse plans to introduce a standard community for tokenized deposits by the primary half of 2027.

The Worldwide Financial Fund mentioned the impression of tokenization is prone to lengthen far past funds. Tobias Adrian, director of the IMF’s Division of Monetary and Capital Markets, mentioned future coverage selections will decide whether or not tokenization makes the monetary system extra environment friendly or creates new fragmentation.

associated: $60 billion tokenized RWA market reveals no on-chain exercise, report finds