U.S. shares opened with a burst of optimism on Wednesday, however that enthusiasm light by mid-afternoon as stronger-than-expected jobs numbers pushed up Treasury yields and waned hopes for short-term rate of interest cuts from the Federal Reserve.

Wall Avenue’s early pop fades as sizzling jobs knowledge pushes yields up, weighs on inventory costs

On the time of this writing, February 11, 2026, the Dow Jones Industrial Common, after briefly rising greater than 300 factors in early buying and selling, was down about 120 factors, or 0.2%, to round $50,068. The S&P 500 index fell about 0.2% to about 6,928, and the Nasdaq Composite Index fell 0.5% to about 23,000. Markets stay open and intraday fluctuations proceed.

The set off was the non-farm payroll report for January, which was delayed as a result of current authorities shutdown, and confirmed that the variety of staff elevated by 130,000, far exceeding the estimate of practically 50,000. The unemployment price fell from 4.4% to 4.3%, strengthening the view that the labor market stays sturdy.

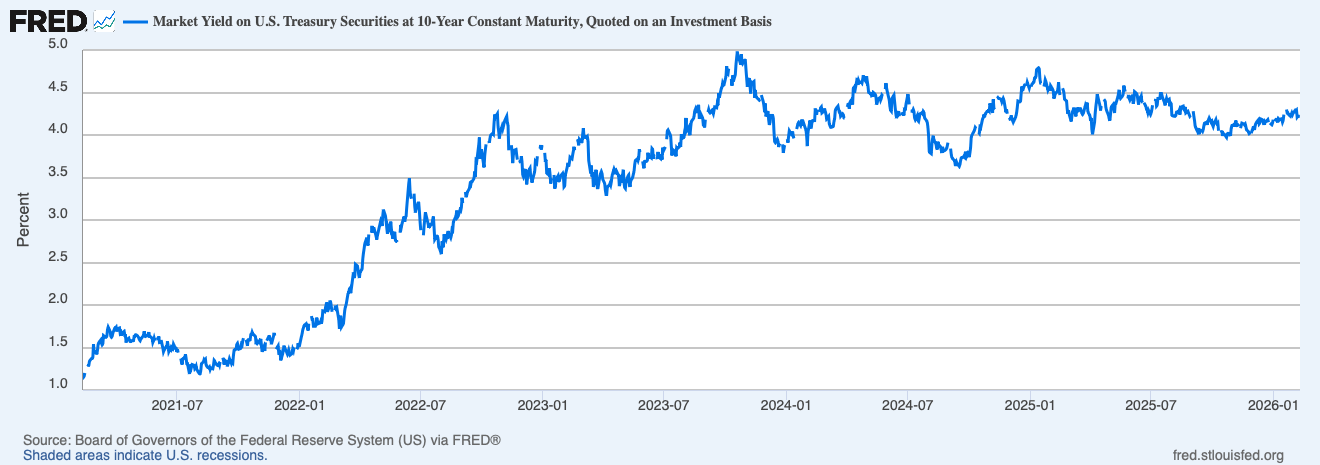

That power had its pitfalls. Authorities bond costs fell, and the yield on 10-year bonds rose to about 4.22% from about 4.18% beforehand. Greater yields usually weigh closely on inventory valuations, particularly in areas of excessive market progress. Merchants are recalibrating their expectations that the Fed will ease in 2026, with restricted rate of interest cuts now factored in and most expectations transferring past mid-year.

The estimated market yield on a 10-year fastened maturity U.S. Treasury invoice, on an funding foundation, represents the annualized return an investor would require to carry a 10-year U.S. Treasury bond, expressed as a share of its worth reasonably than its face worth.

The reversal marks a change from Tuesday’s shut, when the Dow Jones Industrial Common set a three-year report of fifty,188.14. Nevertheless, the S&P 500 and Nasdaq closed decrease, reflecting stress from weak retail gross sales knowledge and selective profit-taking in tech shares.

Earnings season added additional cross-currents. Vertiv Holdings rallied sharply after reporting a optimistic outlook associated to knowledge heart demand, whereas Lyft, Robinhood and Mattel fell after weak earnings and outlooks. Inventory-specific reactions widen sector efficiency disparities, and volatility stays elevated although index-level actions seem modest.

Expertise shares and communications providers shares that led the current advances within the synthetic intelligence (AI) craze have confronted new scrutiny. Monetary shares had been comparatively resilient as rising yields supported internet curiosity margins, whereas vitality shares had been supported by sturdy oil costs amid geopolitical tensions.

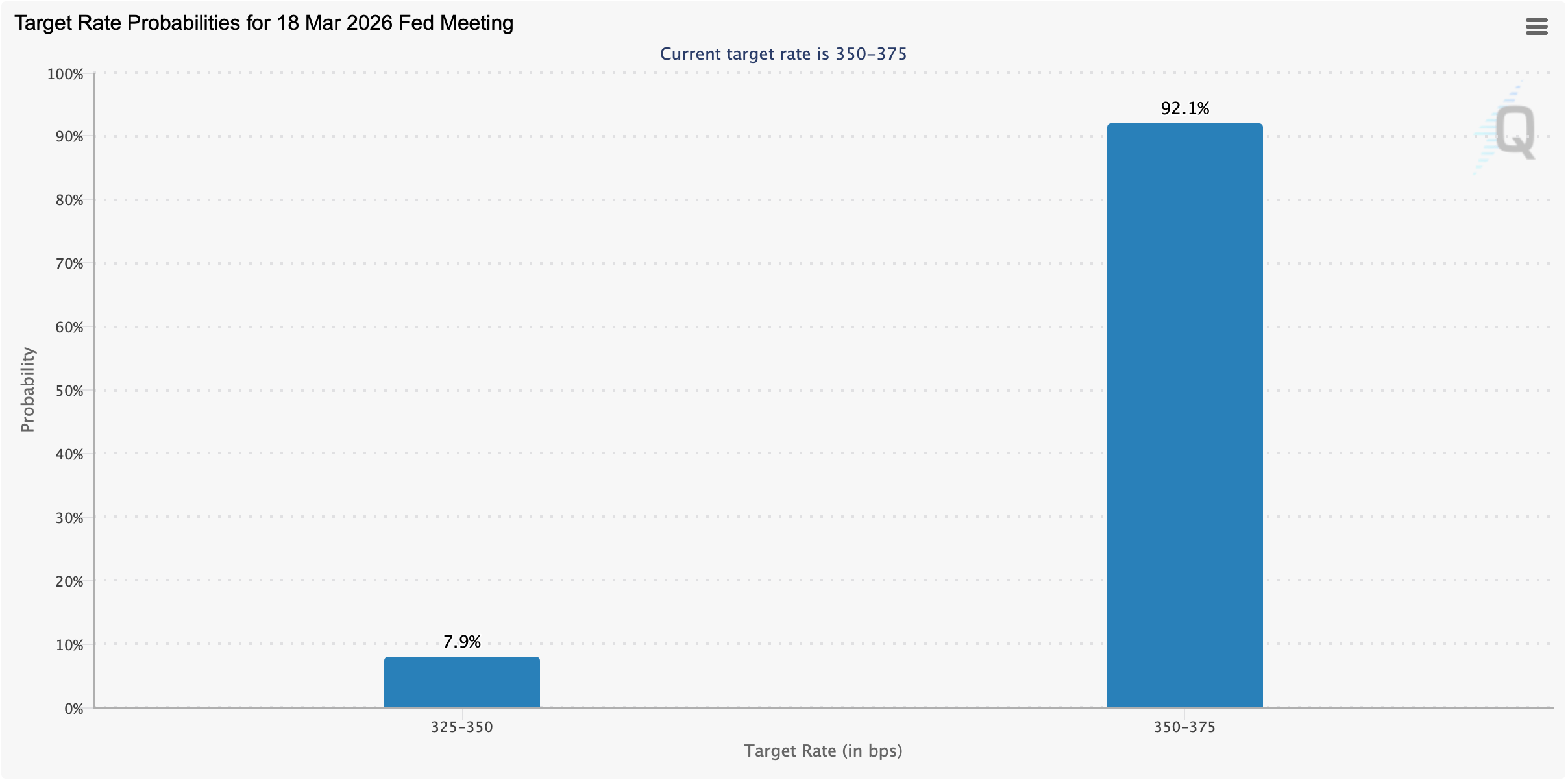

As of Wednesday, February 11, the US Federal Reserve is extensively anticipated to maintain the federal funds price unchanged when policymakers reconvene in 35 days.

Valuable metals comparable to gold and silver rose on Wednesday, with gold rising 0.66% to above the $5,000 degree. Silver was buying and selling at $83 per ounce, up 2.43% from yesterday. Like U.S. shares, the cryptocurrency economic system has fallen, with the sector falling 3.2% to $2.28 trillion by noon. Bitcoin has fallen 3.8% in opposition to the greenback over the previous seven days.

Trying forward, Friday’s Shopper Worth Index (CPI) report will doubtless be the spotlight occasion of the week. Inflation knowledge might both strengthen the “long-term excessive” narrative or reopen the door to early rate of interest easing. evaluationsts expects fourth-quarter earnings progress for the S&P 500 index to be near 12%, with forecasts for 2026 anticipated to be within the mid-teens, however these assumptions are topic to secure inflation and regular demand.

For now, the market message is obvious. Robust financial knowledge is welcome, however not if it complicates the Fed’s path. With the CPI on observe and income nonetheless beginning to roll in, Wall Avenue seems poised for extra intraday whiplash earlier than the week ends.

Incessantly requested questions 📉

- Why did US shares fall at midday on February 11, 2026?U.S. Treasury yields rose after January’s better-than-expected jobs report, denting expectations for the Federal Reserve’s short-term rate of interest cuts.

- How do authorities bond yields have an effect on the inventory market?Rising yields will enhance borrowing prices, placing stress on inventory valuations, particularly for growth-oriented shares.

- Which indexes are underperforming at present?The Nasdaq Composite has fallen far behind the Dow and S&P 500.

- What would be the subsequent main catalyst for the market this week?Friday’s Shopper Worth Index (CPI) knowledge might form expectations for inflation and Federal Reserve coverage.